CalPERS Admits Massive Bets In Dicey Private Equity

- PAUL PRESTON

- 3 days ago

- 4 min read

Jun 15, 2026

California Public Employee Retirement System (CalPERS) as largest U.S. public pension plan with $563 billion under management, just disclosed that its recent amazingly high reported investment performance came from concentrating 21% of all pension assets in potentially dicey “private equity.”

CalPERS has a long history of private equity (PE) investment scandals. From 2009 to 2015, board member Alfred Villalobos and CalPERS CEO Federico Buenrostro split tens of millions in fees and bribes to steer tens of billions of investment dollars toward private equity firms (notably Apollo Global Management) that invested in failed Chinese buy-outs.

Mountain Top Times' Substack is a reader-supported publication. To receive new posts subscribe in the box below. To support my work, consider becoming a paid subscriber.

Villalobos and Buenrostro were charged with fraud by the SEC for allegedly falsifying disclosure documents. Villalobos was also federally indicted on corruption and bribery charges, but amazingly died just before trial opening.

CalPERS retirees in May 2026 released a detailed new report by forensic expert Edward Siedle alleging CalPERS’ systemic PE risks included:

· Secrecy and lack of transparency — withholding key information from beneficiaries, and public regarding complex alternative investments;

· Chronic underperformance — bottom 15% of U.S. public pension funds over 5- and 10-year periods;

· Understated costs and excessive fees — hidden or misreported fees paid to external managers; and

· Conflicts of interest and governance failures — questionable board oversight and staff practices.

CalPERS responded on June 15th with a 68-page report stating the pension fund had adopted a new strategy in 2022 that concentrated 40% of all new investments in PE. As a result, the fund now has 132 private equity managers investing $119.3 billion, or 21.1%, of all the fund’s assets.

CalPERS also reported phenomenal PE returns in the last 3 years [below], claiming its spectacularly high PE returns increased its funding status, which allowed the state to legally reduce billions of annual contributions.

CalPERS claimed that its private equity had lower risks and higher returns than stock and bonds because their new hiring focus was on Emerging and Diverse Managers” that through “Environmental, Social, and Governance (ESG) integration” would achieve higher “Structural Alpha” outperformance.

But according to the Federal Reserve, private equity default risk is higher than traditional investments due to “PE firms typically finance acquisitions with substantial debt—often 5–7x EBITDA or higher in leveraged buyouts (LBOs)—secured against the target company’s assets and cash flows. This structure creates financial distress risk if revenues or margins weaken, as fixed interest obligations strain liquidity.”

The Federal Reserve pointed to a Moody’s Credit Rating Service study that PE-backed firms defaulted at roughly 14-17% between 2022–2024, twice the rate of non-PE-backed speculative-grade companies.

The Fed did acknowledge that some academic and historical analyses did suggest PE ownership can mitigate risk through operational improvements and lower asset volatility, leading to comparable or even lower default probabilities after controlling for leverage.”

But the Fed emphasized that in downturns or high-rate environments, leverage magnified downside risks.

According to the Private Equity Bankruptcy Tracker for 2025:

· “Private equity firms played a role in 54% (19 out of 35) of the largest U.S. corporate bankruptcies during 2025 (bankruptcies with liabilities of $1 billion or greater at the time of filing).

· Private equity firms played a role in 51% (21 out of 41) of large U.S. corporate bankruptcies during 2025 (bankruptcies with liabilities of $500 million or greater at the time of filing).

· Private equity firms played a role in 10% (39 of 388 filings) of all corporate bankruptcies in 2025, despite the fact that private equity accounts for only 7% of the U.S. economy.

· According to S&P data, private equity firms played a role in 44% (18 out of 41) of distressed exchanges, which are out-of-court debt exchanges that allow companies to circumvent a formal bankruptcy process, but are often accompanied by similar outcomes to those seen in bankruptcies.

· The impact of private equity ownership is notable in specific sectors. In manufacturing, private equity-backed companies accounted for 60% (3 of 5) of the largest bankruptcies.

· In the largest consumer discretionary bankruptcies, private equity-backed companies account for 71.43% (5 of 7), including brands like Joann Fabrics, At Home, and Claire’s.

· Private equity-backed companies account for 44% of the largest (4 of 9) healthcare bankruptcies in 2025. These bankruptcies are especially devastating to consumers and may leave people without access to essential care.

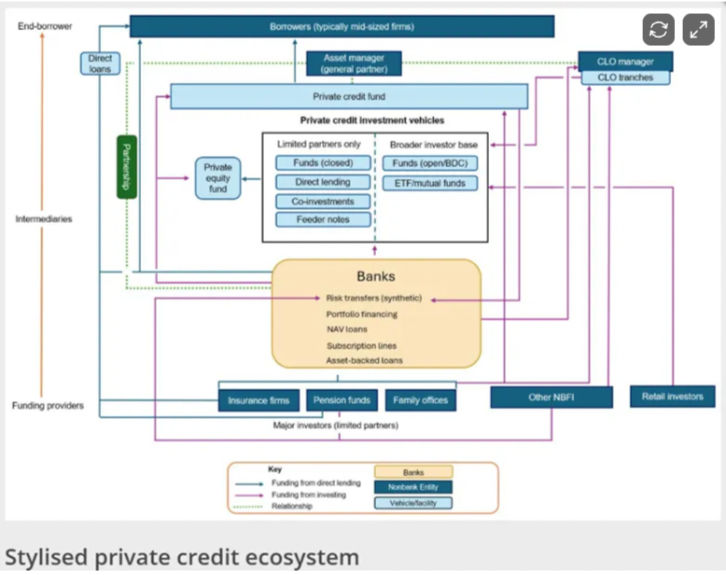

Global private equity funds at 2024 year-end were estimated at $1.5–2 trillion. But the Financial Stability Board (FSB) that promotes global stability, reported in May 2026 that: “U.S. banks have committed roughly $300–322 billion in lending to PE and private credit sponsors (via subscription lines, NAV loans, and warehouse facilities)—a roughly 30-fold increase since 2013.” FSB demonstrated that “additional exposures arise from direct lending to portfolio companies and CLO holdings.” [below]

FSB also warned that U.S. insurance companies have allocated up to a third of the pension assets they manage into private credit. Due to this Multiple Leverage Layers and Concentration, private equity losses could be amplified and “liquidity pressures could transmit across balance sheets.”

The CalPERS private equity report was meant to reassure its pension participants and auditors that: “Nothing to see here, move along.” But this risky sub-prime lending sounds like the run-up to the 2008 Financial Crisis.

Mountain Top Times' Substack is a reader-supported publication. To receive new posts, subscribe in the box below. To support my work, consider becoming a paid subscriber.

Comments